Accounts Receivable | Credit Management

Credit limit at the SO. Not at FY-end review.

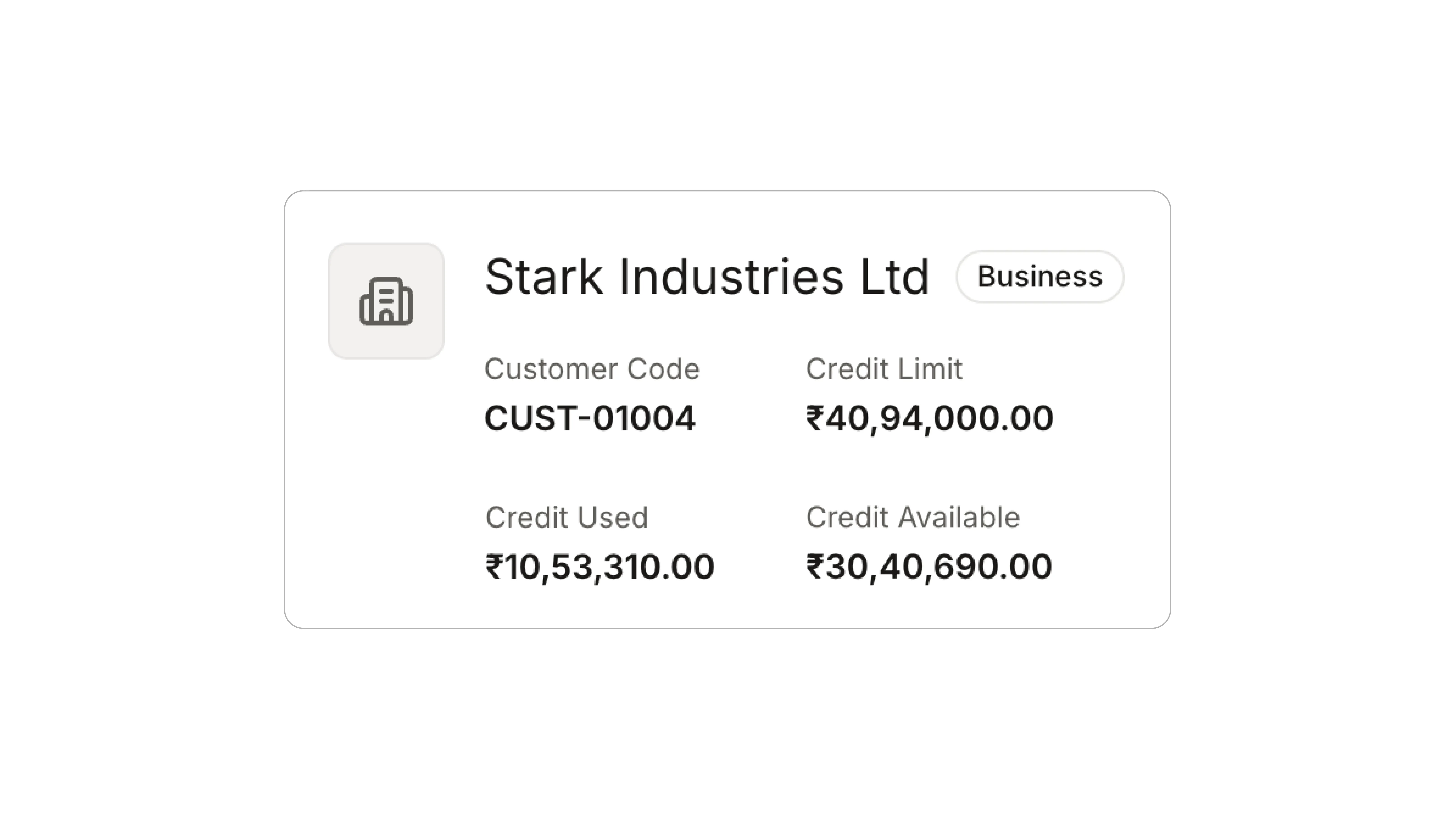

Per-customer credit limits set on the customer record. Live utilisation across open SOs, open invoices and open receipts. Breach blocks the next SO with a CFO override path. Exposure aging flagged per bucket. The trigger fires before despatch, not after the cheque has bounced.

What the system does

Capability, input, output.

| Capability | Input | Output |

|---|---|---|

| Per-customer credit limit | Customer + risk tier + limit | Limit + approval matrix |

| Live utilisation | Open SOs + invoices + receipts | Available credit, real-time |

| SO block | New SO + available credit | Allow / block / override path |

| Aging exposure | Customer outstanding by bucket | Risk flag on customer record |

| Override capture | CFO override + reason | Audit trail with approver |

| Concentration view | All customers + outstanding | CFO concentration dashboard |

-

Per-customer credit limit

- Input

- Customer + risk tier + limit

- Output

- Limit + approval matrix

-

Live utilisation

- Input

- Open SOs + invoices + receipts

- Output

- Available credit, real-time

-

SO block

- Input

- New SO + available credit

- Output

- Allow / block / override path

-

Aging exposure

- Input

- Customer outstanding by bucket

- Output

- Risk flag on customer record

-

Override capture

- Input

- CFO override + reason

- Output

- Audit trail with approver

-

Concentration view

- Input

- All customers + outstanding

- Output

- CFO concentration dashboard

Compliance + integrations

Credit risk surfaced at the source.

The block fires at SO save, not at audit. The override leaves an audit trail. The concentration view feeds Schedule III credit risk disclosure.

Regulations we work within

-

Schedule III, Part I

Trade receivables aging disclosure pre-populated.

-

Ind-AS 109 (Expected Credit Loss)

ECL provisioning supported with portfolio analytics.

-

Companies Act, Rule 11(g)

Override audit trail captured.

Connects to

- Tally Prime Customer master sync with credit limit

- Credit bureau APIs External credit score feed (CRIF, CIBIL)

Credit Management FAQ

What buyers ask.

Can the credit limit formula be customised?

Yes. Default formula is limit minus open SOs minus open invoices minus open receipts. Configurable to include / exclude open SOs (some teams hold credit only against invoiced amounts), to include / exclude credit notes, and to include / exclude entity-specific items.

CFO override on a credit breach. How does that work?

The override surfaces the breach amount, the customer's aging exposure, and the historical override pattern for that customer. CFO authorises with reason; the override is captured in the audit trail and visible on the customer record.

Can we pull credit bureau scores into the limit decision?

Yes. CRIF and CIBIL APIs are integrated. The bureau score (where available for B2B customers) feeds into the risk tier. Limit recommendations are surfaced at customer onboarding and at periodic review.

How does this play with Ind-AS 109 ECL provisioning?

The customer aging buckets, payment behaviour and bureau scores feed into the Expected Credit Loss model. The ECL provision is computed at portfolio and customer levels per Ind-AS 109. The CA reviews the provisioning before period close.

More in Accounts Receivable

Related features

Customer 360

Quotes, SOs, invoices, receipts, credit limits, contacts and documents on one customer record.

See Customer 360Receipt Allocation

Bank receipts auto-matched to invoices. Advances, partial payments and FX gain/loss inline.

See Receipt AllocationPayment Follow-ups

Automated reminders across email, WhatsApp, call queues. Customer-history-aware tone.

See Payment Follow-ups

Set up credit limits on your top 50 customers.

Connect one entity, free. Configure the limit formula and the override matrix. The first SO breach surfaces the override screen, the audit trail and the concentration view.